At our meeting with lawyers to discuss the HE and Research Bill, we noted that the Bill includes the provision to introduce a method of ‘Alternative Payments’ (sections 78-79). The House of Commons Briefing Paper (pp.39-40) is perhaps the best summary of what is included on this matter in the Bill. What it amounts to is an alternative fund specifically set up to be Sharia-compliant, managed by the Student Loans Company, acting as agents on behalf of the fund.

The idea of a Sharia-compliant form of student finance was put out to consultation by the government in 2014 because they recognised that “student loans issued after September 2012 bear a real rate of interest above inflation and concerns have been raised that some religious groups, particularly Muslims, may feel that the charging of such an interest rate is incompatible with their beliefs.” Following the consultation, the government settled on the proposal of a ‘Takaful fund’. Here’s how they describe it. It’s worth quoting in full:

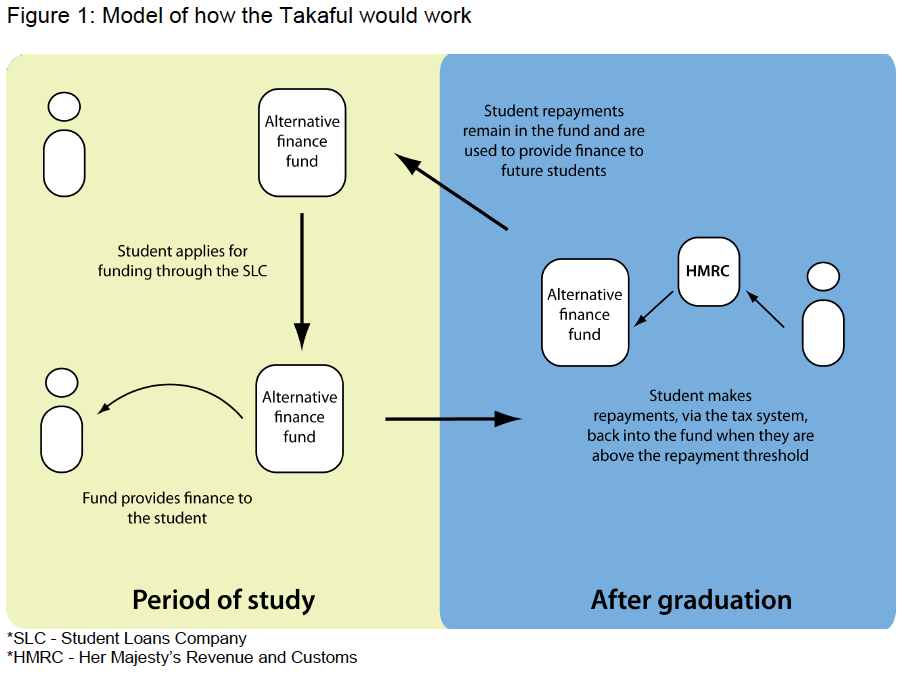

“The suggested Alternative Finance model’s underlying principle is one of communal interest and transparent sharing of benefit and obligation, with the repayments of students participating in the fund being used to provide finance to future students who select to join the fund. This ensures that all members of the fund benefit equally from it…

… The finance product the Government identified is based on the ‘Takaful’ structure used in Islamic finance to allow groups of people to cooperate to provide mutual finance assistance to members of the group. This type of mutual fund model is familiar to Sharia scholars and many UK Muslim families, who use a similar concept to raise funds between cooperating relatives.

Students participating in the fund would not be borrowing money and paying it back with interest to a third party, which would not be compliant with Sharia law. Instead, the Takaful fund will be established with an initial amount of money that can be donated to the fund or on the basis of Qard Hasan (interest-free loan) and based on a concept of mutual participation and guarantee.

Students will obtain finance from the fund by applying in a similar manner to the conventional loan. The contract will be based upon a unilateral promise guaranteeing that they will repay a Takaful contribution – which is perceived as a charitable contribution from a Sharia perspective for the benefit of the members of the fund. Monies will be released once the contract is signed. Repayment will be made to the fund once they are in employment and earning above the repayment threshold, which would be set at the same level as for traditional student loans.

The contribution paid back into the fund by the student would help future students benefit from the fund, allowing them to complete their studies as the original student did. The mutual basis of this structure, with members (borrowers) of the fund helping each other to attend higher education, would make this model acceptable under Sharia-law. This is because the lending/borrowing relationship which results in a payment of interest by the students to the Student Loans Company does not exist in this model.

The student finance fund, i.e. the Takaful fund, would be managed by a fund manager (in this case the Student Loans Company under the Islamic finance principle of Wakala (agency) for a specified fee. The fund would be completely segregated from the traditional student loans to ensure full compliance with Sharia in the whole cycle of the fund.”

Although the principle driver behind this new alternative fund is to accommodate Muslim students, the way it is then translated into the White Paper and eventual HE&R Bill is stripped of any reference to being Sharia-compliant because it is the values and principles on which the fund is established and operates, rather than specific religious beliefs that will define it, hence why it’s referred to as ‘Alternative Finance’ and not ‘Sharia-compliant Finance’.

Those principles, according to Wikipedia are the following:

Policyholders cooperate among themselves for their common good.

Policyholders contributions are considered as donations to the fund (pool)

Every policyholder pays his subscription to help those who need assistance.

Losses are divided and liabilities spread according to the community pooling system.

Uncertainty is eliminated concerning subscription and compensation.

It does not derive advantage at the cost of others.

“Theoretically, takaful is perceived as cooperative or mutual insurance, where members contribute a certain sum of money to a common pool. The purpose of this system is not profits, but to uphold the principle of “bear ye one another’s burden”.”

“takaful is founded on the cooperative principle and on the principle of separation between the funds and operations of shareholders, thus passing the ownership of the Takaful (Insurance) fund and operations to the policyholders. Muslim jurists conclude that insurance in Islam should be based on principles of mutuality and co-operation, encompassing the elements of shared responsibility, joint indemnity, common interest and solidarity.”

As the government describe in their report on the initial consultation, this is a co-operative mutual fund of communal interest, and as described in the HE White Paper (pp.59-60), the fund will be open to anyone and result in exactly the same payments as the existing loan system, albeit established on different principles:

“To ensure participation and choice are open to everyone, we will introduce an alternative student finance product for the first time. This will be open to everyone and will not result in any advantage or disadvantage relative to a student loan, but will avoid the payment of interest, which is inconsistent with the principles of Islamic finance. We plan to legislate for the Secretary of State to offer an alternative student finance product alongside his current powers to offer grants and loans.”

Illustration from the government’s consultation response document.

The Equality Analysis of the HE&R Bill (p.36), also recognises that while it is principally of interest to Muslim students, “No particular group of students should be worse off as a result of the policy”, likewise underlining the fact that this ‘alternative product’ may appeal to anyone.

“Overall, the policy addresses a potential barrier to entry faced by some potential students, and should lead to an increase in higher education participation. No particular group of students should be worse off as a result of the policy, and the most significant gains will be felt by Muslim students.”

The interesting question this raises for me is to what extent will the co-operative movement ‘endorse’ this form of State-funded method of student finance, given the 4th principle of ‘autonomy and independence’ (usually meaning from the State)? How compatible is it with established co-operative principles of mutualism? I see that the International Cooperative and Mutual Insurance Federation (ICMIF) promote Takaful insurance using the .coop domain name. This suggests that existing Takaful funds are recognised as operating according to the Co-operative movement’s values and principles. The question remains to what extent the new government fund will actually be a ‘co-operative pool’ for the ‘common good’ of its ‘members’? On the face of it, if I were a student deciding which form of State finance to apply for, I would choose the ‘Alternative Finance’ and become a member of the ‘communal pool’, if only because it sounds more ethical.

One thought on “A ‘co-operative mutual fund of communal interest’ for student finance?”

Great to explore this. The limits of what the Government is proposing from a coop perspective is that there is no member control and there is a risk that any fund is not truly independent and autonomous. ICMIF, as you point out, has done good work on pointing to how co-operative forms of Takaful can work, but they might caution that not all Takaful schemes are run on this basis. Great blog!

Great to explore this. The limits of what the Government is proposing from a coop perspective is that there is no member control and there is a risk that any fund is not truly independent and autonomous. ICMIF, as you point out, has done good work on pointing to how co-operative forms of Takaful can work, but they might caution that not all Takaful schemes are run on this basis. Great blog!

Ed